Banking

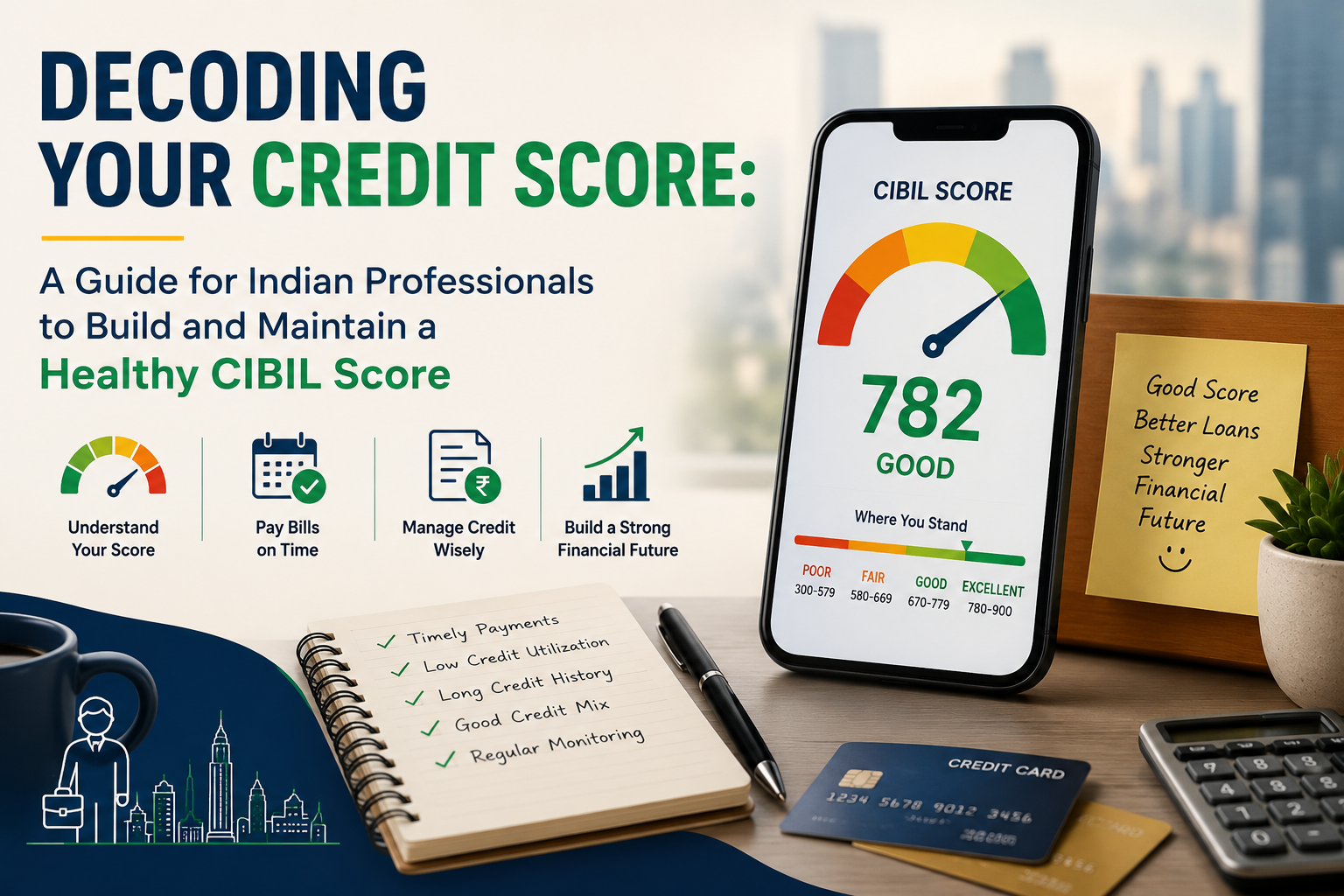

Decoding Your Credit Score: A Guide for Indian Professionals to Build and Maintain a Healthy CIBIL Score

Navigating the complexities of personal finance is a crucial skill for every Indian professional. Among the many financial metrics, your CIBIL score India stands out as a foundational element, acting as a financial passport that dictates your access to credit. For those aiming for home loans, car loans, or even a simple credit card, understanding, building, and maintaining a healthy CIBIL score is non-negotiable.

What is a Credit Score and its Paramount Importance in the Indian Financial Landscape?

A credit score is a three-digit numerical summary of your creditworthiness, ranging typically from 300 to 900. In India, the CIBIL Score (provided by TransUnion CIBIL) is the most widely recognized and used credit score. It's a snapshot of your past credit behaviour, including your borrowing and repayment history.

Why is this score paramount for Indian professionals?

- Access to Credit: Lenders (banks, NBFCs) primarily use your CIBIL score to assess your eligibility for loans and credit cards. A higher score signals lower risk.

- Favourable Terms: A good CIBIL score can unlock lower interest rates on loans (like home loans or personal loans) and higher credit limits on credit cards, saving you substantial money over time.

- Faster Approvals: Loan applications with strong credit scores often experience quicker processing and approval times.

- Beyond Loans: In some cases, landlords might check your credit score before renting out property, and certain employers, especially in finance-related roles, might conduct background checks that include credit history.

How Your CIBIL Score is Calculated: A Breakdown of Key Influencing Factors

Your CIBIL score isn't a random number; it's a meticulously calculated figure based on data collected from various lenders. Here are the primary factors that influence your CIBIL score India:

- Payment History (Approx. 30-35%): This is the most critical factor. Consistent, on-time payments of EMIs (Equated Monthly Instalments) for loans and credit card bills positively impact your score. Any default or delay can severely damage it.

- Credit Utilisation (Approx. 25-30%): This refers to the amount of credit you're using compared to your total available credit limit. A high utilisation ratio (e.g., using 80% of your credit card limit) is seen as a sign of credit dependency and can lower your score. Aim to keep it below 30%.

- Credit Mix and Type (Approx. 15-20%): A healthy mix of secured loans (like home or car loans) and unsecured loans (like personal loans or credit cards) is generally preferred. Having only unsecured credit might be viewed less favourably.

- Length of Credit History (Approx. 10-15%): A longer credit history with good repayment behaviour demonstrates responsible credit management over time, which benefits your score.

- New Credit Applications (Approx. 10%): Each time you apply for new credit, a 'hard inquiry' is made on your credit report. Too many applications in a short period can suggest desperation for credit and negatively impact your score.

Debunking Common Myths and Misconceptions Surrounding Credit Scores

Many myths circulate around credit scores, leading to unintentional mistakes. Let's clarify some for Indian professionals:

- Myth 1: Checking my CIBIL score will lower it.

- Reality: This is largely false. Checking your own score (a 'soft inquiry') does not impact it. Only 'hard inquiries' by lenders when you apply for new credit affect your score.

- Myth 2: Having no credit history means a perfect credit score.

- Reality: Lenders prefer to see a track record of responsible borrowing. Zero credit history (a "Credit Score -1" or "NA") makes it difficult for lenders to assess your risk, often leading to loan rejections or less favourable terms.

- Myth 3: Closing old, unused credit cards is good for my score.

- Reality: While it might seem logical, closing old cards can reduce your total available credit, thereby increasing your credit utilisation ratio (if you have other active cards) and shortening your credit history length – both potentially negative impacts.

- Myth 4: Only CIBIL matters; other bureaus are irrelevant.

- Reality: While CIBIL is dominant, India has three other major credit bureaus: Experian, Equifax, and CRIF High Mark. Lenders might use data from any or all of these. It's wise to be aware of your standing with all.

Practical and Actionable Tips to Effectively Improve Your Credit Score

Improving your CIBIL score India is a journey of consistent, disciplined financial habits. Here are actionable steps:

- Pay Your Dues On Time, Every Time: This is the golden rule. Set up reminders, auto-debits, or calendar alerts for all your EMIs and credit card bill due dates. Even a single missed payment can significantly hurt your score.

- Maintain Low Credit Utilisation: Aim to use no more than 30% of your available credit limit on credit cards. For example, if your credit limit is ₹1,00,000, try to keep your outstanding balance below ₹30,000.

- Build a Healthy Credit Mix: A balanced portfolio of secured loans (e.g., home loan, car loan) and unsecured loans (e.g., personal loan, credit card) is beneficial. Avoid having too many unsecured loans initially.

- Limit New Credit Applications: Apply for credit only when genuinely needed. Spreading applications across multiple lenders in a short span makes you appear credit-hungry and can trigger multiple hard inquiries, lowering your score.

- Regularly Review Your Credit Report: Obtain your free credit report annually from CIBIL or other bureaus. Check for any errors, fraudulent accounts, or inaccuracies. Rectifying these can quickly improve your score.

- Be Patient and Consistent: Building a strong credit score takes time. There are no shortcuts. Consistent good behaviour over several months and years will gradually reflect positively.

- Start Building Credit Early (If You Have None): If you're new to credit, consider getting a secured credit card (against a fixed deposit) or a small, easily repayable personal loan to establish your credit history.

The Direct Impact of a Healthy Credit Score on Loan and Credit Card Approvals

A robust CIBIL score India isn't just a number; it's a powerful tool that directly influences your financial opportunities:

- Higher Approval Chances: Lenders are more likely to approve loans and credit cards for individuals with high scores (typically 750+), as they are perceived as reliable borrowers.

- Lower Interest Rates: A good score can qualify you for the best interest rates on home loans, car loans, and personal loans. For instance, a difference of even 0.5% on a large home loan can save lakhs over its tenure.

- Increased Credit Limits: Credit card companies are more inclined to offer higher credit limits to cardholders with excellent credit histories.

- Better Terms and Conditions: You might gain access to premium credit cards with better rewards programs or more flexible loan repayment terms.

- Faster Loan Processing: Banks often fast-track applications from individuals with strong credit profiles, reducing waiting times significantly.

How to Check Your Credit Score for Free in India: Available Resources

Checking your CIBIL score India regularly is a prudent financial habit. Fortunately, there are several ways to do this for free:

- TransUnion CIBIL Website (cibil.com): You are entitled to one free full credit report from CIBIL every year. This is the official source.

- Other Credit Bureaus: Experian, Equifax, and CRIF High Mark also offer one free credit report annually on their respective websites.

- Financial Aggregator Platforms: Many popular Indian fintech platforms and financial aggregators like BankBazaar, Paytm, PhonePe, Google Pay, and even some official bank apps (e.g., HDFC Bank, ICICI Bank) offer free CIBIL score checks. While these might not always provide the full detailed report, they give you the score and often key influencing factors.

Strategies for Maintaining a Robust Credit Profile for Sustained Financial Growth

Building a good CIBIL score India is one thing; maintaining it for long-term financial health is another.

- Automate Payments: Set up auto-debits for all EMIs and credit card bills to ensure you never miss a due date.

- Budgeting and Financial Planning: A solid budget helps you manage your finances, ensuring you have funds available for loan repayments and avoids over-reliance on credit.

- Monitor Credit Usage: Keep an eye on your credit card spending and ensure it remains well within the 30% utilisation threshold.

- Regularly Review Credit Reports: Make it a habit to check your credit report at least once a year from each bureau to catch and rectify errors promptly.

- Avoid Co-signing Loans Blindly: When you co-sign a loan, you become equally responsible for its repayment. A default by the primary borrower will also impact your CIBIL score.

- Educate Yourself Continuously: Stay updated on credit policies and best practices. Financial literacy is your best defence against credit pitfalls.

By diligently following these practices, Indian professionals can cultivate and maintain an exemplary CIBIL score India, paving the way for greater financial freedom and unlocking superior opportunities in the country's dynamic financial landscape.

Disclaimer: This article is intended for informational and educational purposes only and does not constitute financial or investment advice. Readers are encouraged to consult with a qualified financial advisor before making any financial decisions. Lumic.co.in does not guarantee any specific financial outcomes.